Perc Pineda, PhD

Chief Economist, Plastics Industry Association

What might appear as a soft improvement in plastics product manufacturing in March—a 0.7% increase from February and a 0.5% decline from a year ago—continues to reflect underlying softness in manufacturing. However, at the level of output, production has increased over the last five consecutive months. It is difficult to ascertain whether the recent monthly increases are the beginning of a sustained rise in plastics product manufacturing.

Recent manufacturing trends and plastics production

Other manufacturing metrics, such as the Institute for Supply Management’s (ISM) PMI, have shown improvements. In March, the U.S. Institute for Supply Management’s Manufacturing PMI® was in expansion territory at 52.7—the third consecutive month above the growth threshold of 50.[1] In fact, the second quarter opened with the PMI holding steady at 52.7 in April,[2] following a 10-month period of contraction. This improvement adds to the overall strengthening of manufacturing indicators.

The latest Gardner Business Intelligence plastics processing data indicate a resilient U.S. plastics industry, remaining above the growth threshold for the fourth consecutive month in April, with an improving outlook supported by new orders and future business metrics. The production component rose to 62.7, reversing declines from 57.6 in February to 56.3 in March and marking the highest level since March 2021.[3]

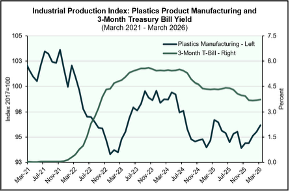

Long-term data on plastics production show manufacturing hovering around 2017 levels—reaching a 3.6% increase in November 2021 but falling 6.8% compared to 2017 levels as interest rates crossed above 4.0%, as shown in the accompanying chart below. Weak manufacturing activity resulting from changes in U.S. policy slowed plastics production—manufacturing is the major market of the plastics industry, after all.

From emergency stimulus to monetary tightening

According to the U.S. Government Accountability Office, Congress enacted approximately $4.65 trillion in COVID-19 relief funding through multiple laws passed in 2020 and 2021. Against the backdrop of pandemic-related supply chain disruptions, fiscal and monetary policy were firing on all cylinders to support the economy, generating both demand-pull and cost-push inflation simultaneously. Demand surged due to massive fiscal stimulus and near-zero interest rates, while pandemic-related supply disruptions pushed producer prices higher.

As inflationary pressures intensified, monetary policy shifted from expansionary to contractionary, resulting in rising interest rates. The Federal Reserve System began hiking the federal funds rate—the benchmark interest rate influencing short-term rates—from a 0%–0.25% target range in March 2020 at the onset of COVID-19 lockdowns to 0.25%–0.50% in March 2022. It increased further, reaching 4.75%–5.00% a year later. By July 2023 through August 2024, the target range reached 5.25%–5.50%. The Federal Reserve began cutting rates in September 2024 with a 50-basis-point reduction. By December 2025, rates had declined to 3.50%–3.75% and have remained at that level since.

Interest rates and trade policy as constraints on production

Plastic products manufacturing is sensitive to short-term interest rates both directly and indirectly. Major capital expenditures in plastics manufacturing—such as equipment—rise and fall with borrowing costs. Major end markets of the plastics industry, such as construction, motor vehicles, and light trucks, are also interest-rate sensitive. Thus, plastics production reacts to changes in monetary policy through both direct and indirect channels. As shown in the chart below, as interest rates rose—illustrated using the 3-month Treasury bill yield—plastics manufacturing began to decline. Additionally, any short-term rebounds in production were not sustained. From late 2023 through 2024, plastics production has trended downward.

What appeared to be a reversal in the downward trend in plastics production was cut short as trade and tariff policy conditions shifted. While higher tariffs have had an uneven effect on the plastics industry, they have weighed on the cost of imports. From a trade and tariff policy perspective, it is not tariffs per se that are the issue, given that international trade has existed for centuries and tariffs have long been used as policy tools. Rather, the focus should be on the optimal tariff rate that avoids reducing economic welfare—particularly consumption and production outcomes. Additionally, tariffs alone cannot single-handedly revive domestic production, which for many industries is a long-term goal rather than a short-term reality. Regulatory relief, tax incentives, and policies supporting workforce supply and development are also important components.

While recent indicators might suggest stabilization in manufacturing activity and a gradual improvement in the plastics industry, the recovery remains uneven, below its long-term trend, and sensitive to changing financial conditions. Given continued pressure on capital investment and interest-rate-sensitive end markets, interest rates may need to come down further to support a more durable and broad-based recovery in manufacturing and plastics production. The plastics industry remains resilient, but the pace and durability of recovery will depend on monetary policy, manufacturing activity, and broader economic conditions in the months ahead. These broader conditions, against the backdrop of evolving tariff policy and ongoing geopolitical conflict, will also influence the outlook for the plastics industry.

[1] Institute for Supply Management, “Manufacturing PMI® at 52.7%; March 2026 ISM® Manufacturing PMI® Report,” PR Newswire, April 1, 2026, https://www.prnewswire.com/news-releases/manufacturing-pmi-at-52-7-march-2026-ism-manufacturing-pmi-report-302730721.html

[2] Institute for Supply Management, “Manufacturing PMI® at 52.7%; April 2026 ISM® Manufacturing PMI® Report,” PR Newswire, April 2026, https://www.prnewswire.com/news-releases/manufacturing-pmi-at-52-7-april-2026-ism-manufacturing-pmi-report-302759226.html

[3] Perc Pineda, PhD, “Numbers in Perspective,” Gardner Business Index: Plastics Processing, Plastics Technology, https://www.ptonline.com/search?q=Perc%20Pineda.stakeholders are also encouraged to visit the USITC website to submit comments directly or reach out to PLASTICS to have their perspectives represented.

While the first six months of 2022 brought economic contraction causing production to move sideways…

Assessing the plastics industry landscape in 2023 reveals a year marked with nuanced shifts across…