Perc Pineda, PhD

Chief Economist, PLASTICS

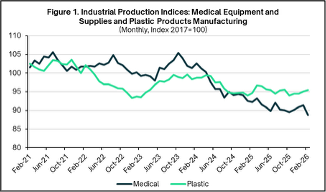

The U.S. production of medical equipment and supplies, as measured by the Industrial Production Index, was 5.6% above its 2017 base year level in July 2021. At the end of the COVID-induced recession in April 2020, production was 19.7% below 2017 levels, before surging 31.5% above 2017 levels by July 2021. Production then moderated, with notable increases such as 4.8% in August 2022. After a 2.1% decline in May 2023, consecutive monthly gains brought production 5.4% above the 2017 base in October 2023, followed by a subsequent decline of 15.7% from that recent peak as of February 2026.

Healthcare Spending Remains Strong

In the United States, healthcare expenditures have remained around 16–17% of inflation-adjusted personal consumption expenditures (PCE) since 2007, rising to 18% last year. Such consistently high shares suggest that spending on healthcare—which topped $2.9 trillion in 2025—is unlikely to decline anytime soon. Meanwhile, spending on pharmaceuticals and other medical products, which use plastics and packaging, has remained steady at 3–4% of real PCE since 2007, valued at $663.2 billion in 2026.

What can the plastics industry take away from falling U.S. medical equipment and supplies production since October 2023?

Post-Pandemic Normalization and Inventory Correction

The Industrial Production Index (IPI) for medical equipment and supplies, tracked by the Federal Reserve, covers products in NAICS 3391, which includes establishments primarily engaged in manufacturing medical equipment and supplies for hospitals, physicians, dentists, and other healthcare providers. Plastics are widely used in this industry, including in diagnostic apparatus, laboratory equipment, syringes, catheters and related disposables, as well as in surgical and medical instruments, surgical appliances, dental equipment, ophthalmic goods, orthopedic devices, prosthetics, and artificial body parts.

However, plastics and plastic products in this sector are tracked separately under NAICS 3261 (Plastic Products Manufacturing), which includes medical and dental plastics finished products and plastic packaging materials and containers. As shown in Figure 1, the Industrial Production Indices for these two industries follow different trends: while medical equipment and supplies experienced a prolonged post-COVID production surge, plastics manufacturing had a shorter elevated run, helping explain why declines in plastics demand have been less pronounced. The clearing of high COVID-related inventories weighed on production in NAICS 3391—and by extension, affected demand for plastics to some extent.

Import Competition Despite Higher Tariffs

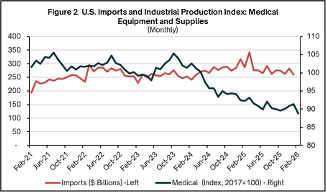

Foreign medical devices and components have partially replaced U.S.-made products. As shown in Figure 2, the value of imports of medical equipment and supplies remained flat through 2025, despite exposure of certain products to Section 232 steel and aluminum tariffs under Chapters 90 (medical instruments), 94 (hospital furniture), and 84–85 (machinery/electrical equipment for medical settings). Products with metal housings/components, such as diagnostic or surgical instruments, are directly exposed to the Section 232 derivative lists[1].

By contrast, plastics consumables—including PPE, apparel, masks (HTS 3926), components such as tubing (HTS 3917), device parts (HTS 3926), and packaging like bags, bottles, and sterile containers (HTS 3926)—are not subject to Section 232 derivative tariffs, insulating these segments from the impact of metal-focused duties.

A pickup in domestic production could occur depending on how long slower elective procedures persist, a trend noted by industry observers in 2023. Financial market analyses also highlight that hospitals are navigating financial headwinds and cost pressures, which influence decisions on capital equipment purchases. Future interest rate cuts could, perhaps, help prevent further deferrals of these purchases, supporting domestic production.

Looking ahead, the supply side of medical equipment and supplies is bifurcated, with stable imports but lower domestic production, while demand remains solid. From a strategic perspective, businesses should focus on the global value chain of medical equipment and supplies production, with particular attention to longer-term prospects. This supply-demand imbalance is reflected in prices: the Producer Price Index (PPI) for medical equipment and supplies manufacturing shifted from a declining trend between February and August 2025 to an upward trend from September 2025 through February 2026 (year over year). However, the index pulled back slightly in January and February 2026, reaching 2.9% year over year, down from 3.1% in December 2025.

[1]The Section 232 derivative list contains personal and healthcare goods such as pharmaceutical products for retail, though these would not necessarily be captured under medical equipment and supplies production as designated by NAICS 3391.