Perc Pineda, PhD

Chief Economist, Plastics Industry Association

The U.S. economy is famously consumer-driven. Personal consumption expenditures (PCE) make up roughly 69% of gross domestic product (GDP). Yet while consumer spending grabs most of the headlines, Gross Private Domestic Investment (GPDI) plays a disproportionately important role in long-term growth and productivity.

In Q4 2025, GPDI reached $5.5 trillion (seasonally adjusted annual rate), accounting for about 17-18% of GDP. Within that investment pool, spending on industrial equipment — from CNC machines and injection molders to industrial molds and specialized processing machinery — is especially critical.

However, higher tariffs on steel, components, and finished machinery have increased costs and created uncertainty for manufacturers. One important mitigating factor: the permanent restoration of 100% bonus depreciation under the 2025 One Big Beautiful Bill Act. This tax provision significantly lowers the after-tax cost of new equipment and gives businesses a strong incentive to invest despite higher upfront prices.

The Role of GPDI in the Economy

GPDI measures business spending on fixed assets (structures, equipment, and intellectual property) plus changes in private inventories. Nonresidential fixed investment in equipment is especially dynamic. It drives innovation, boosts worker productivity, and supports manufacturing reshoring.

In 2025, real GDP grew 2.1%, with investment playing a meaningful role alongside consumer spending. However, equipment investment faces headwinds: higher interest rates earlier in the cycle followed by higher tariffs contribute to supply chain related uncertainties, and now tariffs. Industrial equipment categories — including metalworking machinery and special industry machinery not elsewhere classified (n.e.c.) — are particularly sensitive because, in addition to domestic manufacturing, machines and their components are imported into the United States come from other countries.

Zooming In on Industrial Equipment

According to BEA classifications, industrial equipment includes:

These assets power key sectors of U.S. manufacturing, including automotive, packaging, medical devices, and consumer goods. Plastics manufacturers, for example, depend heavily on both processing machines (classified under special industry machinery) and precision molds (classified under metalworking machinery).

Recent data show a mixed but resilient picture: overall equipment investment posted modest growth in late 2025, supported by AI infrastructure, automation, and onshoring, with spending on special industry machinery rising solidly to $52.3 billion in Q4 2025 (up from $45.8 billion a year earlier), while investment in metalworking machinery dipped slightly to $29.0 billion, down from $30.2 billion in Q4 2024. Even so, ongoing tariff pressures threaten to slow this momentum.

Tariffs Raise the Cost of Capital

2025 tariffs on steel, aluminum, electronics, and machinery from major trading partners have increased input costs for domestic equipment makers and importers. Heavy equipment manufacturers reported hundreds of millions to billions in added tariff costs in 2025, with similar impacts expected in 2026. For a mid-sized plastics processor, a 10-25% tariff on imported molds or extruders can significantly delay or cancel planned capital projects.

Higher upfront costs reduce return on investment (ROI) and extend payback periods. This is especially painful for small and medium manufacturers operating on thin margins. Without a policy response, tariffs risk dampening the very investment needed for supply chain resilience and productivity growth.

The Power of Permanent 100% Tax Expensing

Fortunately, tax policy provides a strong countermeasure. The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, permanently restored 100% bonus depreciation for qualifying property acquired and placed in service after January 19, 2025. IRS Notice 2026-11 provided clarifying guidance, confirming the rules.

How it works: Businesses can deduct the full cost of eligible new or used equipment in the year it is placed in service, rather than spreading depreciation over 5, 7, 10, or 20 years. This applies to most industrial machinery, molds, and equipment with recovery periods of 20 years or less.

Key advantages:

For plastics manufacturers and other industrial firms, this covers both processing machinery and the molds themselves.

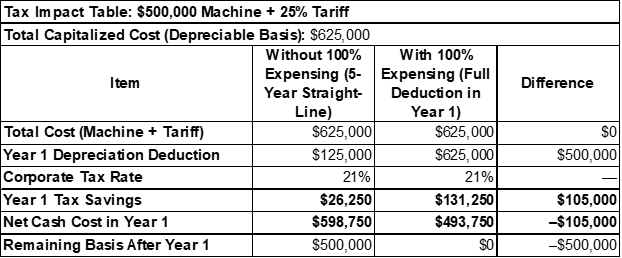

How Expensing Offsets Tariff Costs: A Simple Example

Consider a $500,000 imported injection molding machine facing a 25% tariff based on customs value. The tariff adds $125,000, bringing the total cost to $625,000.

Bottom line: The immediate tax benefit largely offsets the tariff hit, shortening the payback period and improving ROI. Many businesses effectively reduce the tariff’s bite by 30-40% or more when factoring in time value of money. This incentive encourages companies to accelerate purchases, invest in domestic or near-shore alternatives, and modernize operations.

Broader Implications and Outlook

Permanent 100% expensing supports the manufacturing renaissance by making capital investments more attractive even amid trade tensions. It complements other policies aimed at reshoring and automation. Early evidence suggests that permanent 100% tax expensing helped prevent a sharper decline in equipment investment, including on imported machinery, despite higher tariffs in 2025, which had an uneven impact across the plastics industry value chain, as shown in the chart below. For instance, despite higher tariffs, imports of injection molding machines under HTSUS 8477109030 rose by 315 units—705 in 2024 to 1,020 in 2025. There were also 345 units increase in injection molding under HTSUS 8477109060, and 742 units increase in blow molding machines, HTSUS 8477300000, over the same period.*

Under the One Big Beautiful Bill, 100% first-year expensing primarily benefits eligible depreciable capital assets, while a separate provision allows immediate deductions for domestic R&D and research expenditures, which are not traditional depreciable assets. Policymakers should consider complementary measures like enhanced domestic production incentives to maximize U.S. manufacturing growth.

For manufacturers, the 2026 policy environment is likely to be an important window for reassessing capital investment plans, particularly in light of 100% bonus depreciation for qualifying tangible asset purchases placed into service after January 19, 2025. From a cost-of-capital perspective, accelerated depreciation can improve the after-tax return on investment for machinery, molds, and automation, with potential implications for productivity and competitiveness over the medium to long term.