Perc Pineda, PhD

Chief Economist, Plastics Industry Association

The United States–Mexico–Canada Agreement (USMCA) includes a provision requiring the three countries to jointly review the free trade agreement six years after it enters into force. Since USMCA took effect on July 1, 2020, the first scheduled review will take place this year. On May 28 and 29, the United States and Mexico had its first round of talks in Mexico City. Prior to the bilateral talks, the U.S. Plastics Industry Association (PLASTICS) and Mexico’s National Association of Plastics Industries (ANIPAC) issued a joint statement indicating their full support for the extension and expansion of the free trade agreement.The next round of bilateral negotiations will take center stage on June 16 and 17 in Washington, D.C.

USMCA trade performance

The interdependence between the United States, Mexico, and Canada, which has been enhanced by the USMCA free trade agreement, is evident in the volume of trade between these three countries. Between 2016 and 2025, U.S. exports to both countries increased by 2.81% CAGR to $510.7 billion. Meanwhile, U.S. imports from both countries reached $917.0 billion in 2025 – as imports rose by 5.4% CAGR over the same period. All told, the U.S. had a $406.2 billion trade deficit with its USMCA trade partners.

When analyzing international trade, viewing it solely through the lens of the aggregate trade balance—defined as a nation’s total exports minus its total imports—proves incomplete and potentially misleading. Economists have long argued that a focus on trade surpluses can be misleading, since economic gains come primarily from specialization, comparative advantage, and the benefits of exchange rather than from the trade balance itself. In the balance of payments framework, trade deficits are often offset by capital inflows, reflecting foreign investment in the domestic economy. However, these inflows are not uniformly beneficial: when they primarily finance public debt for current consumption rather than productive investments, they can crowd out private capital formation, elevate long-term debt burdens, and contribute to slower growth, as suggested by the twin deficits hypothesis and documented in a large body of empirical research on debt overhang and economic growth.

Looking beyond overall trade totals and focusing on detailed industry and product-level data provides a clearer view of a country’s competitiveness, its areas of comparative advantage, and the specific demand patterns of its trading partners. For instance, the United States recorded a $12.7 billion trade surplus in resin and plastic products (Harmonized System Chapter 39) with Mexico and a $1.7 billion surplus with Canada in 2025. These surpluses underscore strong North American integration and regional demand under the USMCA. Mexico and Canada are the largest export markets for the U.S. plastics industry, supported by the deeply interconnected manufacturing supply chains of the three countries. Because plastics serve as a critical intermediate input across a wide range of manufacturing industries, the integration of North American production networks help sustain robust cross-border trade in plastics materials and products. Together, the three economies generated a combined GDP of $27.8 trillion in 2025.

The case for extending and expanding USMCA

From the plastics industry’s perspective, three primary reasons stand out for continuing and expanding the USMCA: regional competitiveness, national security, and employment opportunities. In an era marked by the growing importance of regional trade agreements, economic cooperation among neighboring countries remains a key driver of sustained growth. For this reason, the USMCA should not only be preserved but expanded to strengthen North American economic integration, enhance regional competitiveness, and promote long-term prosperity.

Competing trading blocs underscore the urgency of this approach. The Regional Comprehensive Economic Partnership (RCEP), comprising 15 Asian economies that account for 30% of global GDP and over a quarter of the world’s exports,[1] represents the world’s largest trading bloc. The European Union, with its 27 members, forms the world’s third-largest economy, with a GDP estimated at 18.0% of global GDP[2], after the United States and China. Meanwhile, the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) covers 14.4% of global GDP[3] and includes overlapping members with RCEP, such as the United Kingdom, Mexico, and Canada. Although the United States maintains 14 free trade agreements in force covering 20 countries, the priority should be on fine-tuning and deepening these agreements—particularly USMCA—to bolster competitiveness across industries, not only domestically but across the North American region, while building more resilient supply chains.

The COVID-19 pandemic starkly demonstrated the critical importance of reliable supply chains for U.S. manufacturing. Exogenous shocks that disrupt global networks create both market disruptions and national security vulnerabilities. Reshoring and nearshoring production—within the United States and to adjacent USMCA partners—helps mitigate these risks by ensuring more reliable access to essential manufactured goods, including resin and plastic products.

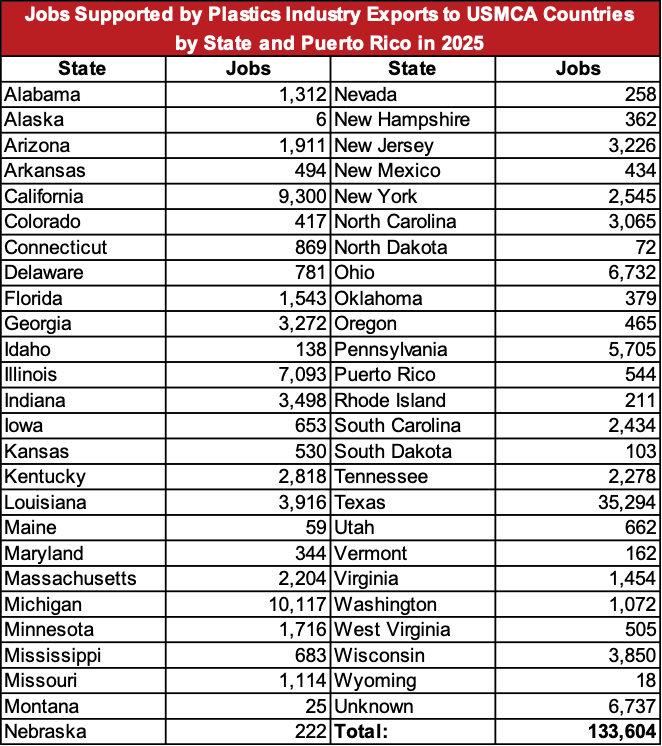

Finally, international trade serves as a powerful engine for job creation. The plastics industry, a key supplier to the broader manufacturing sector, directly employs over one million U.S. workers and supports millions more across downstream industries. Plastics exports to USMCA partners alone supported approximately 133,604 U.S. jobs in recent data (see Table), highlighting the agreement’s role in sustaining employment throughout the regional supply chain.

The path forward

As the USMCA review process advances, policymakers should seize this opportunity to extend and strategically expand the agreement. Doing so will reinforce North America’s position as a competitive, resilient, and self-reliant manufacturing powerhouse. By deepening regional integration, the United States, Mexico, and Canada can better counterbalance larger global trading blocs, safeguard critical supply chains, protect American jobs, and deliver sustained economic benefits for the plastics industry and the millions of workers and manufacturers it supports. The evidence from both aggregate trends and sector-specific successes strongly favors a bolder, forward-looking USMCA.

Table

[1] Regional Comprehensive Economic Partnership (RCEP). https://asean.org/our-communities/economic-community/integration-with-global-economy/regional-comprehensive-economic-partnership-rcep/

[2] World Economic Outlook. International Monetary Fund. www.imf.org

[3] Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). https://www.dfat.gov.au/trade/agreements/in-force/cptpp/background-documents